The future looks bright for the Indian CV industry despite the disruptions. Shyam Maller looks at how the ecosystem is buckling up for FY2022 and keeping the wheels moving.

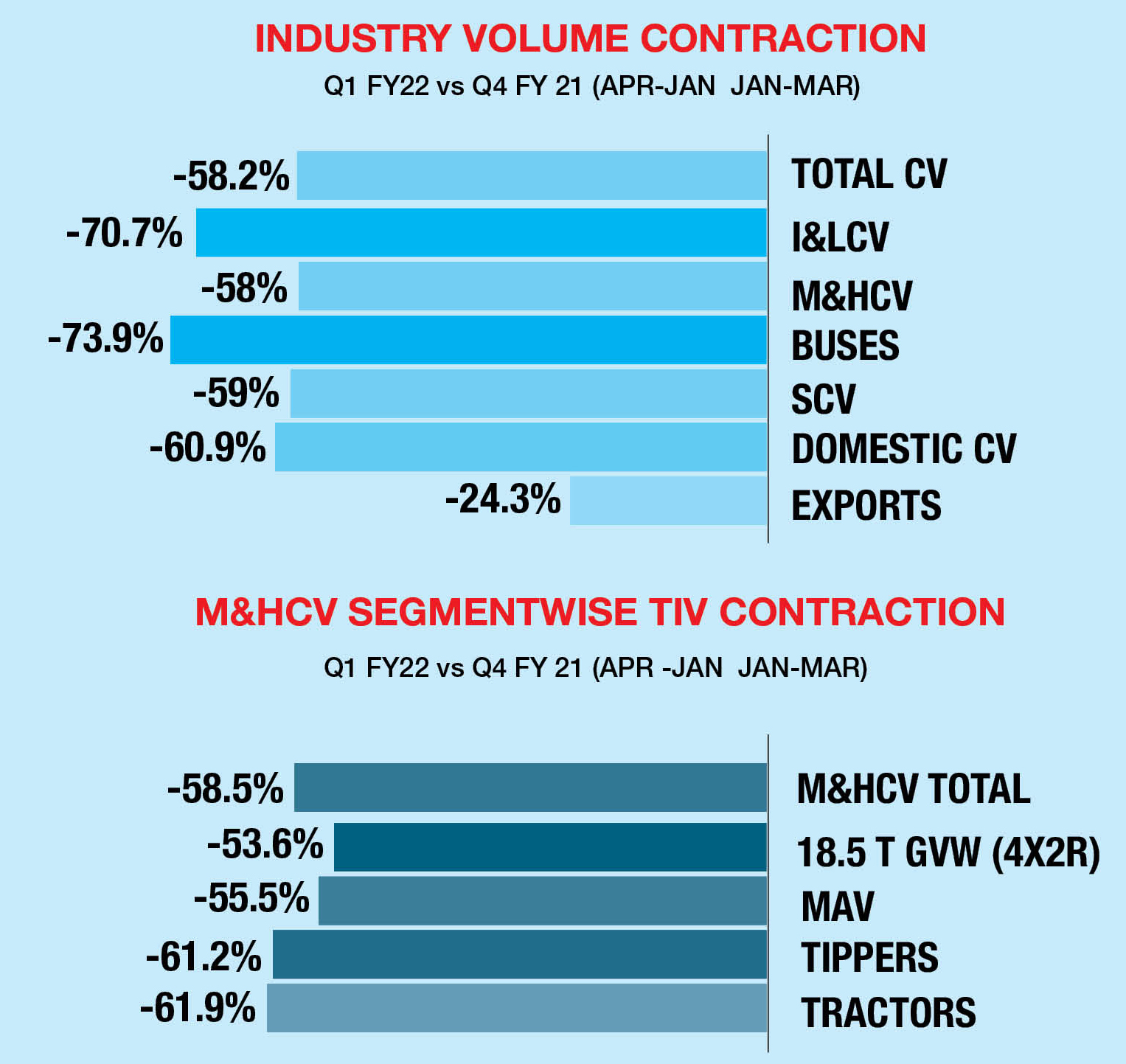

The last three years have brought torrid times for the CV industry and the cohorts in the ecosystem. The Covid-19 pandemic that was a veritable final nail in the coffin for businesses in FY2021, has continued to torment the industry into the first quarter of the financial year 2022 (Q1FY22) as well as through the second wave of the pandemic. The Q1FY22 (Apr-Jun’ 2021) sales were down by nearly 61 per cent compared to Q4FY21 (Jan-Mar 21). (Refer to Chart A).

There have been truly very significant lessons that have been learnt of managing resources with better speed, quality, cost optimisation leading to better efficiency and productivity. Going forward, it is critical to broaden and deepen the transformation that has been kickstarted and particularly with the impending transition from diesel to new fuels including the transition to electrification and hydrogen fuel cells. The skill sets and the strategy to navigate and lead in the ‘New Normal’.

So, let’s take a peek at what bodes for us and the CV industry in the year ahead and what are the areas that we need to be cognizant of and strategise actions.

Rise of digital

Every adversity, hidden therein, is an opportunity waiting to be tapped. The pandemic, as it engulfed us fast-forwarded the adoption of digital. It accelerated customer acquisition through online and digital marketing. It helped better engagement with customers, improved lead generation effectiveness, enhanced Customer Experience (CX) in the virtual mode via quicker responses and resolution of customer complaints.

About 23 per cent of marketers looked at digital transformation as a new channel for customer outreach and nearly 48 per cent said it was for outreach including sales, marketing and service. Companies are now using analytical models at every stage of the purchasing cycle viz from lead generation, product recommendation to customers, sales forecasting, customer retention to name a few. Customer segmentation is further honed to the customer persona level and when it is integrated into the customer life cycle, it can yield excellent results in the form of better lead conversion. Post pandemic, companies have moved away from the generic media options and successfully leveraged digital thereby significantly optimising and improving customer experience as well as the cost of customer acquisition. And as we emerge out of the pandemic, phygital (the means to bridge the physical world with the digital aimed at providing unique interactive experiences) will be the new mantra for companies and channel partners. Investment into reskilling of the sales force as well as in the service workshop area ,both at the OEM’s and at dealerships to embrace digital tools will only facilitate higher productivity and lower the staff costs .

Large, swanky showrooms are going to witness scaling down and smaller touchpoints are expected to proliferate. The disruptive model of the “agency sales” of dealerships are going to gain currency. With a clear objective of offering seamless customer experience across brick and mortar worlds, ensuring a consistent brand salience and most importantly price transparency. Original Equipment Manufacturers (OEMs) and dealerships, particularly post-pandemic are rethinking their sales structure and network strategies faced with increasing competitive pressure, rising costs and thinning margins.

eCommerce: Co-creating for growth

The E-retail market is expected to continue its strong growth – it registered a CAGR of over 35 per cent to reach Rs.1.8 trillion (USD 25.75 billion) in FY20. Over the next five years, the Indian e-retail industry is projected to exceed an estimated 300-350 million shoppers, propelling the online Gross Merchandise Value (GMV) to USD 100-120 billion by 2025. The Indian online grocery market is estimated to reach USD 18.2 billion in 2024 from USD 1.9 billion in 2019, expanding at a CAGR of 57 per cent. India’s e-commerce order volumes increased by 36 per cent in the last quarter of 2020. As a result, this mega business not only offers scope for trucks (SCVs) for the last mile distribution but also for cargo vehicles from LCVs, ICVs as well as M&HCVs.

The MNC players like Amazon and Flipkart who straddle the e-Com market have outlined their serious intentions to adopt EVs and this is an opportunity that Auto OEMs are ( and have to work ) working closely with and co-create transportation solutions. There is a flurry of activity around three-wheeler EVs with companies like Mahindra, Piaggio jostling with technology startups like Euler Motors, Altigreen etc. for offering efficient and affordable last-mile logistics solutions. Clearly for these MNC’s, it is about ESG and aspiring to be ahead of the curve when it comes to carbon neutrality and zero emissions. Critical to the success of eV companies will be how they go beyond just the product and the entire ecosystem around it to quell the various concerns and anxiety around electric mobility, the cost, performance and TCO metrics.

Following three-wheelers in the EV space will be last-mile SCVs like Tata Ace that is expected to electrify the segment( pun intended). However, technology and the cost of batteries besides the charging infrastructure will need to be addressed and in this direction, the OEMs will have to piggyback on partnerships with technology startups.

Construction and mining—Digging deep

Tippers, and particularly, multi-axle tippers have been the leading variants in the M&HCV segment in FY21 accounting for nearly 41.5 per cent of the total TIV. And with the massive infrastructure investments by the government as well as vibrant growth in the steel and cement sectors, CV OEMs should be doubling down on engaging with the key players in this segment. Vehicle reliability that translates into uptime will be a significant differentiator for CV brands. This segment will once again be (in tandem with MAVs) leading the resurgence of M&HCV growth in the coming two to three years. The trucks for this sector in BSVI have got more robust and powerful in terms of power and torque besides being more reliable and durable, segmentwise.

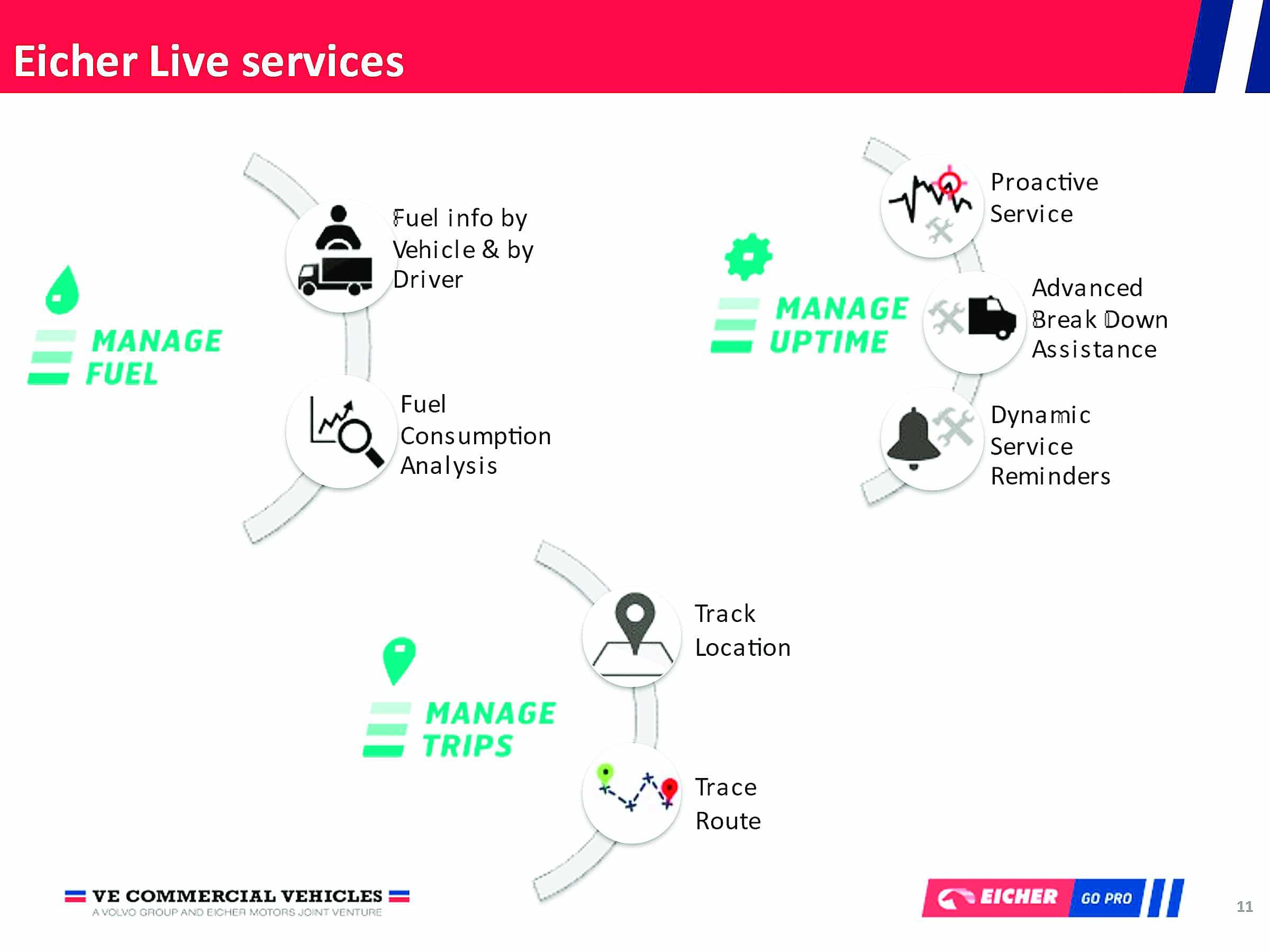

Connected trucks and uptime promise

Connected trucks and uptime promise

BSIV and BSVI trucks are technologically more advanced than their predecessors and are equipped with an advanced Engine Management System (EMS) consisting of ECU/ECM and a plethora of sensors for the driveline and exhaust. The truck can be remotely linked through telematics and allows customers to check and analyse vital vehicle information in real-time via an online portal, including vehicle location and health, besides fuel mileage, ad blue consumption etc. Fleet managers can optimise driver performance, improve fuel efficiency, and reduce downtime.

Fleet operators will want the OEM to provide them with an insight into what the vehicle life-cycle cost will be, and in-tune with their business and the application area in which their vehicle is deployed. This will lead to further digitisation. Connected CVs and a host of services supporting digitisation will grow. This would include real-time driver training and driver behaviour monitoring; geo-fencing, fuel consumption, safety and security, preventive maintenance among others.

Those OEMs that can speedily customise a robust Application Programming Interface (API) for their customers will be at an advantage. An API allows the customer to secure information, data and insights through connectivity. For sensitive applications like pharma, vaccine, perishable and refrigerated goods, connectivity is already proving to be of much importance, in line with the reliability of fleets on asset efficiencies. Predictive maintenance and remote diagnostics, that alerts a driver in time and before any failure will be a major differentiator for an OEM in living up to the promise of maximum uptime and seen as an immense value by fleet operators.

Higher tonnage MAV haulage trucks to lead the way

Consequent to the implementation of GST and the emergence of large warehouses across strategic locations of the country, the Hub and Spoke model has accelerated the adoption and sale of heavier multi-axle trucks. If we analyse the MAV truck sales in 2018-19, 2019-20 and 2020-21, there is clear evidence that the 42-tonne and 49-tonne GVW MAVs have gained ascendancy over the 28-tonne and 35-tonne GVW. The 42-49-tonne GVW segment accounts for close to 50 per cent of the overall haulage MAV segment sales. A similar transition is seen in the construction/soft mining tippers where the 6×4 tippers ( 28.5-tonne GVW) are seeing a shift to 8×2 tippers (35-tonne GVW). The primary driver for this transition being the favourable cost per tonne per km for the higher GVW trucks.

Leveraging aftermarket differentiation and responsiveness

In these extenuating circumstances, OEM’s and dealers will need to invest further into digitisation to raise their service standards as well as upskill their technicians to deliver the First Time Right (FTR) diagnosis and repair. With CV OEMs pushing for long term maintenance contracts and time-guaranteed repairs, dealers will have little alternative but to invest in delivering a heightened customer experience. They will also be prudent to invest in smaller, satellite facilities to increase their customer reach. There is anecdotal data that has been gathered from almost the entire spectrum of CV dealerships that the workshop business has in several places even crossed the pre-pandemic levels. Surely, the more organised dealerships are focusing on getting the aftersales absorption ratio to cross the 85 per cent level ( the aftersales absorption ratio shows a dealership how much of the company’s fixed costs are covered by aftersales revenue).

Gas is the future

India’s commitment to the Paris pledge, to reduce carbon footprint by 33-35 per cent from its 2005 levels by 2030 is cast in stone. On the one hand, while the two-wheeler, three-wheeler and car segments are gravitating towards BEVs, PHEVs, the CV segment especially and the I&LCVs are ideally expected to switch to CNG in the short/medium term. The growing footprint of CNG stations is now expected to spread from the North to the West and down South. CNG stations are expected to grow from the current level of 2200 stations to 10,000 over the next eight to 10 years and the current user base of 3.5 million vehicles will surge to new highs. The Govt is aiming to make gas account for 15 per cent of the energy mix by 2025 from the current level of 11 per cent.

The natural gas demand is set to grow significantly at a CAGR of 6.8 per cent till 2030. It is estimated that CNG penetration in Light & Medium Duty (LMD) trucks is expected to rise from nine per cent of the TIV to about 30 per cent by 2030. OEMs are vying with each other to offer CNG trucks beyond the conventional five, seven, nine, 12-tonne GVW and expand to 16-tonne GVW trucks. With CNG priced at Rs.49.40/kg compared to Diesel at Rs.97.45/litre in Mumbai, it is a no brainer for truck operators in regional distribution to switch to CNG trucks.

The natural gas demand is set to grow significantly at a CAGR of 6.8 per cent till 2030. It is estimated that CNG penetration in Light & Medium Duty (LMD) trucks is expected to rise from nine per cent of the TIV to about 30 per cent by 2030. OEMs are vying with each other to offer CNG trucks beyond the conventional five, seven, nine, 12-tonne GVW and expand to 16-tonne GVW trucks. With CNG priced at Rs.49.40/kg compared to Diesel at Rs.97.45/litre in Mumbai, it is a no brainer for truck operators in regional distribution to switch to CNG trucks.

In FY21, CV OEMs have seen the share of sales of CNG I&LCV trucks ( five to 16-tonne GVW) catapult in double-digit and it now constitutes nearly 45 per cent of total sales of I&LCV. This segment is once again in FY22 expected to report double-digit growth in FY22 as well and the be the segment to watch out for.

For Long haul trucks, and incorporating the learnings from the boom in LNG Heavy Duty trucks in China, the Govt. of India through GAIL, Petronet LNG and the public sector oil companies is investing Rs.10,000 crores to set up 1000 LNG stations on the Golden Quadrilateral (GQ) across major highways, industrial corridors and mining sector over the next three years. This will require the OEM’s to develop larger engines to power trucks and buses for interstate long haul operations. As part of the green makeover of long haul trucks and buses, the govt has set a target of moving eight to 10 lakh trucks and buses ( either new or retrofitted ) to LNG by 2035.

Not only is LNG environmentally friendly with literally nil sulphur dioxide emissions while nitrogenous emissions are sharply reduced by 85 per cent. As compared to CNG, LNG refuelling time is shorter and the typical range for a tankful of LNG is nearly 700-750 kms making it suitable for long haul operations. The payback period for the higher initial investment in an LNG truck is between three to four years, given the savings of nearly two lakhs rupees per annum on fuel costs compared to diesel trucks. The operating cost of LNG trucks is expected to lower fuel bills by nearly 40 per cent compared to diesel. It is, therefore, no surprise that large steel, coal and mining companies who have very large trucks and tipper fleets are keen on working with the PSU oil majors to have LNG supplies delivered which can be the lever for conversion of their diesel trucks to LNG.

Shared Mobility and e-buses

FY22 for the bus industry, in all likelihood, will be a repeat of FY21 with the school bus demand aborted due to the ripple effects of the pandemic. And with continued apprehension of travelling in public service, tourist buses till the vast majority of the population is vaccinated, fresh demand for buses will be a challenge. The only silver lining surrounding buses, in FY 22, is the union budgetary outlay of Rs.18,000 crore for State Transport Undertakings (STUs) to induct around 20,000 buses through the PPP model. We will witness more and more STUs opting to switch to CNG buses that not only meet the BSVI emission norms but are also lower on operating costs vis-a-vis diesel and far lower on acquisition cost vis-a-vis electric buses. It will be both technology-intensive and enterprising.

Already one of two STUs is operating CNG buses ( retrofitted ) as also released tenders for conversion of diesel to CNG and operating these buses on an OPEX model. We could also see some of the STUs go in for replacement of the over 15-year-old buses ( under the Scrappage policy ) but that is slated post, April 01’ 2022. In the recent partial modification of the FAME II scheme, Energy Efficiency Services Ltd (EESL) has been mandated to aggregate the demand of nine cities (with greater than four million population) on an OPEX basis. It is intending to bring down the prices of the buses. Fame-II was launched under the National Mission for Clean Mobility to generate demand for hybrid and electric vehicles by way of supporting 7000 e-Buses but as of date 5595 buses are sanctioned for 64 cities and nearly 2000 ebuses are on the roads.

Hydrogen Fuel Cell Vehicles

Heralded as the fuel of the future, Hydrogen is the solution for long-range mobility. A clean fuel with zero emissions. Hydrogen fuel cells are more economically viable than EVs primarily due to the time it takes to refuel an FCEV over the time it takes to charge an EV. Shorter refuelling times means lower downtime costs. Not only this the high energy density of hydrogen makes it particularly suitable for heavy-goods transport vehicles and has a far lesser payload penalty compared to BEVs. Reliance Industries is leading the India H2 Alliance (IH2A) to commercialise hydrogen technology and systems to help develop a net-zero carbon emissions footprint. So, keeping my fingers crossed and hoping to see long-distance trucks and buses on select segments of the GQ start operating by 2024-25 or who knows in even 2023-24.

Envisioning the Future

With a bumpy start to FY22 that saw Q1 volumes crash, the industry has a challenging task to bounce back. With the Covid-19 third wave that is not just imminent but inevitable, the OEMs have a clear task to reignite the demand while fixing the supply chain issues. The positives for the economy and the CV industry are the good monsoon forecast that will fuel rural demand; the massive impetus for infrastructure and road building by the central government; rising production of key core sectors like coal, steel besides cement; exports has been another area that has been surging over the last six months.

However, what can potentially sour the situation besides the impending 3rd wave: Soaring diesel prices, rising inflation and commodity prices stoking vehicle prices besides the sectors derailed by covid like hospitality, tourism and aviation, that will take time to limp back to normalcy. The expectation by most industry watchers is that the CV sector should come back roaring from onwards September of 2021.

…………………………………………………

The author was formerly Executive Vice President- Sales, Marketing & Aftermarket at VE Commercial Vehicles Ltd( A Volvo Group and Eicher Motors JV). The views expressed by the author are his personal opinion and do not necessarily reflect the views of CV magazine

Also, read Hydrogen Fuel Cell CVs