After an extraordinary FY2020-21, the CV industry is up for another extraordinary year it looks like. The second Covid-19 wave at the beginning of FY2021-22 has disrupted the acquired momentum. The macro economic indicators – the RBI’s original GDP growth forecast for FY2021-22 of 10.5 per cent as well as the Q1 FY2021-22 forecast of 26.2 per cent is unlikely to be met. The second Covid-19 wave has diverted attention from the economic revival in terms of the sequential month-on-month growth in most of the high frequency indicators like GST collections and PMI (Purchasing Managers Index). Lockdowns since April 2021 have been the way of life. The ensuing scenario has diverted attention from the rebound in electricity consumption and the rise of digital payments and electronic toll (FASTag) collections at highway toll plazas.

As efforts are made to tackle the second Covid-19 wave, the ground that the CV industry has covered post the first Covid-19 wave has been brought into question. The hard earned sales momentum has abruptly come to a grinding halt. With the second Covid-19 wave unleashing itself in the second week of April 2021, wholesale and retail numbers have crashed. The alarming growth of Covid-19 infections in the rural hinterland has had a profound effect. The direct impact on CV channel partners and transporter community is not hidden. The stock push by OEMs to retail channels in March 2021 has led to a stock build up of up to 45-60 days of inventory. Transporters have seen their utilisation levels plummet. Freight rates have declined – in April the fall was a good 20 per cent. The steep and unrelenting rise in fuel prices haven’t helped matters. The demand for 90 days loan moratorium is not unfounded. Neither is the 90 day interest support sought by dealers from their principals to neutralise their unsold inventory.

The prognosis

A CRISIL report put the CV industry growth at 36 to 38 per cent (at an estimated 577,000 to 589,000 nos.) for FY2021-22 as compared to that of FY2020-21 (at 568,559 nos.). The second Covid-19 wave has led to the revision of those figures, down to 23-28 per cent. As the wave comes under control, M&HCVs – the barometer of economic growth, are expected to be the first to start recovery. They will be backed by revised FY 2021-22 GDP growth of 9.5 per cent forecast by RBI. While M&HCVs have historically led CV industry sales revival in-line with the economic revival, other segments have followed. I&LCVs will thus follow with a slight lag at 15-20 per cent. Next will be the bus segment at 67-72 per cent on a low base. While the risk of the third Covid wave looms large, much of the heavy-lifting, it appears, will be carried by M&HCVs and SCVs.

As various states begin to unlock in a calibrated manner, industry experts have started debating about the nature of recovery. Whether it will be ‘V-shaped, ‘W’-shaped or ‘K’-shaped. The nature of recovery will influence the supply chains and capacity utilisation for sure. It will also have an effect on how OEMs rev up. A glimmer of hope in the short term is the up coming festive season. Much will however depend on the rate of vaccination, mutation of virus and how the regions with less access to healthcare are able to sustain themselves. Also, how well the third wave, if and when it erupts, is managed with minimal damage to life and businesses.

Good news

The 101 per cent monsoon forecast by the IMD (Indian Meteorological Department ) brings some good news. It makes it safer to assume that most part of the country will receive normal to above normal rainfall. The agricultural sector will benefit from this. The rural economy will get a fillip. There will be more disposable income at the hands of the rural populace. Apart from rise in demand for two-wheelers and tractors, rural economy revival will have a positive influence on steel and cement sectors.

The cascading effect of it will reach auto, road construction, and housing and infrastructure sectors. The revival of these sectors will in-turn help the CV industry improve its fleet utilisation, achieve better freight rates. Increasing inbound and outbound logstics needs of the steel and cement sector, and the infrastructure push by government will also generate demand for M&HCVs. It will trigger a positive sentiment in an industry wrought with Covid-19 related disruptions. Another factor that will trigger a positive sentiment is the performance of the exports sector. Some two- and three-wheeler OEMs experienced unusually high export volumes in April-June 2021. The trajectory of export growth is expected to contine for the rest of the fiscal year.

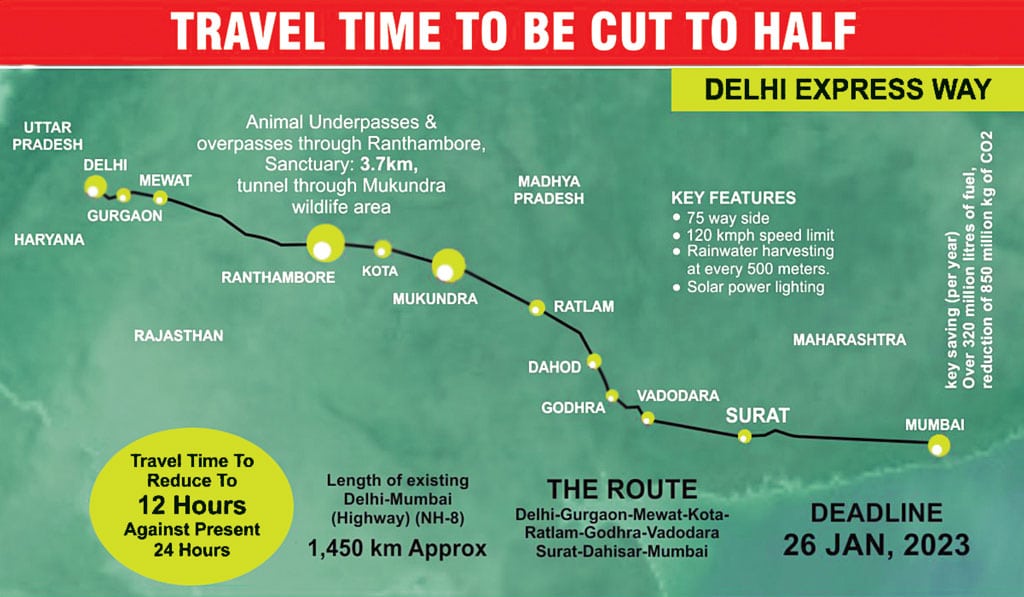

The Bharatmala Pariyojana marks an ambitious lane expansion programme. As greenfield expressways and multi-modal logistics parks further define the hub and spoke logistics arrangement, the National Infrastructure Pipeline Plan with an outlay of Rs.111 lakh crore, from the CV point of view, will help trucks to do higher speed averages and achieve a faster TAT. Spread from FY2019-20 to FY2024-25, the pipeline project has been expanded to include the construction of new roads, rail links, urban infrastructure, etc. A case in point: the Delhi-Mumbai super expressway will significantly improve productivity and revenue earning ability per kilometer covered by halving the travel time.

Fuel prices

and inflation

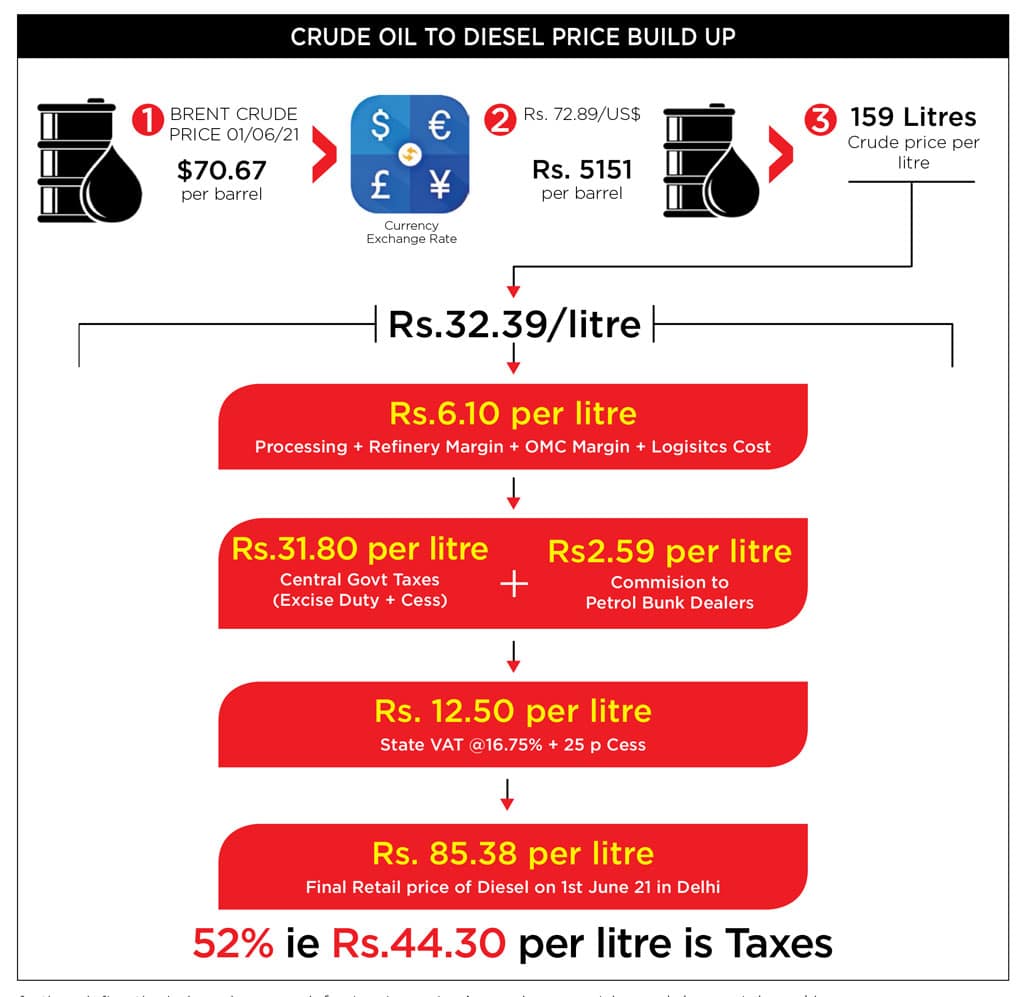

A big challenge for transporters beset by a massive drop in trips and desperately seeking a 90 day moratorium on EMI payments, the runaway fuel prices are puncturing the economic viability of small and medium fleet operators. Diesel accounts for nearly 60 per cent of the operating costs. The illlustration depicts how diesel prices are arrived at. To predict if petrol and diesel prices will be brought under GST and taxed at 28 per cent is tough. The central and state government taxes and excise duty currently account for a whopping 52 per cent (Rs 44.30 per litre of the retail price in Delhi on 1st June) of the Rs 85.38 per litre price of diesel. Claiming to stoke inflation, the continuous rise in fuel prices is elevating challenges for the CV industry in more ways than anticipated. With equated monthly instalments and toll charges forming a big chunk of transporters operating costs, the ferocity of inflation rise could be gauged from the fact that retail inflation rose to 6.3 per cent in May 2021 as against 4.23 per cent in April 2021.

Food inflation rose to five-per cent mark. The wholesale price inflation rose to 12.94 per cent in May 2021. The consumer price index has crossed the six-per cent upper margin set by the Reserve Bank of India (RBI). The RBI, though wanting to keep the interest rates low to support growth, may not be able to do for long. With CV prices having risen nearly 20 per cent in April 2020 due to BSVI transition, another six-to-eight per cent price increase was done by OEM’s in FY2020-21. Another price increase was carried out in April 2021 to adjust the higher input costs. Major influencing factors for OEMs are the fast rising prices of steel and precious metals (like rhodium, palladium, zirconium and platinum). As global markets rebound, fuel and raw material prices are bound to increase further. They are bound to drive small fleet operators out of business. A large swathe of them wound up in last fiscal. Many small and lower retail segment transporters have been badly affected with exposure to market load segment. The less affected are the medium and large fleets that serve B2B logistics clients (with long-term fixed contracts) and e-commerce companies.

Stress in the system

In the CV repair and service space, bigger workshops and authorised dealers have gained at the cost of smaller, unorganised players. The latter’s inability to procure expensive and complex diagnostic tools for BSVI vehicles and perform the necessary upskilling are said to be the reasons. The roll-out of long duration-high mileage warranty and attractively priced AMC schemes have also had an effect. Footfalls at company 3S and 2S dealerships have gone up. At the retail sales level, dealers are tackling the challenge of plummeting volumes since the new axle norms announcement in 2018. Financial indiscipline has forced several dealerships to down shutters permanently. Under pressure to secure channel and inventory finance, dealerships, facing scaling down of inventory funding, are also beset with buyers staring at lower Loan-to-Value (LTV). The turnaround time for ‘proposal-to delivery order (disbursement) have gone up. The benign interest rates are the only solace.

Challenge from Railways

The entire CV ecosystem has come to face an unusual challenge of competition in the form of railways and waterways. The National RailPlan -2030 is one of the many government initiatives to increase freight share of railways from the current 27 per cent to 45 per cent by 2050. Offering lower freight cost, the railways is building Dedicated Freight Corridors ( DFC). It is working to commission by FY2022-23 a total rail length of 2843 km. Connecting major industrial centers in the country, six freight corridors are being constructed. Already dominant in commodity movement (minerals, food grains, petroleum, coal, cement, iron and steel for example), the railways is making inroads into long-haul, cross country movement of cars, tractors and construction equipment. Acquiring multimodal operational abilities to optimise productivity and costs, the railways is also emphasising on ‘Roll-On-Roll-Off ‘ operations (like it just did in the case of oxygen tankers). On a different plane, the scrappage policy – estimated to create a demand for new CVs with a timely replacement of some 37 lakh vehicles above 15 years of age, is falling short of luring truckers. The incenstives are not attractive to say the least. For meaningful results, the government should lower the GST on CVs from 28 per cent to 18 per cent for a period of six to eight months at least.

Summing up

Riding out the Covid induced demand destruction and the devastating domino effect it has had on the entire economy besides the various elements that makes up the CV industry eco system (made up of OEMs, customers, dealers, repair garages, financiers, etc), is going to be a big challenge. Customer needs have changed, and in the post pandemic world, OEMs have had to refocus on the entire value chain as well as improve customer experience in the phygital landscape. And key to success is for the OEMs and the channel partners to work symbiotically with agility and innovation.

…………………………………………………

The author is former Executive Vice President – VE Commercial Vehicles Ltd. The views expressed by the author are his personal opinion and do not necessarily reflect the views of the CV magazine.