The year 2020 was an extraordinary year for the CV industry.

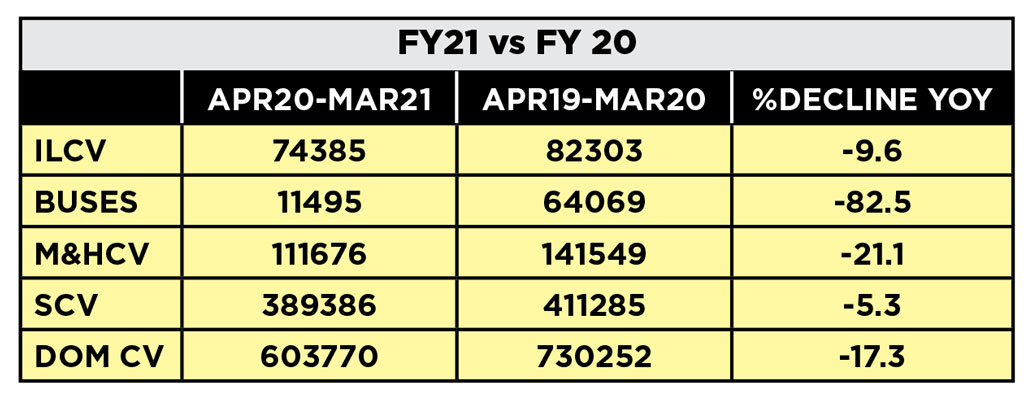

A black swan event for the Indian and world economy, FY2020-21 saw cataclysmic ramifications across businesses, sectors and human lives. Transitioning to BSVI that pushed the prices of vehicles up by 18 to 20 per cent, the CV industry, in FY2020-21 had to deal with the massive body blow of the Covid pandemic. Plagued with excess capacity (mainly due to the new axle norms of 2018) and already experiencing a sales decline post a peak of FY2018-19, the CV industry faced strained finance availability as banks and financial institutions tightened lending policies. Staring at a new world order where things would never be the same again, the CV industry found itself in a situation that looked no less than a gigantic catastrophe. The chart (FY21 vs FY20) aptly highlights what FY2020-21 was like for the CV industry. It puts forth numbers that point at the pain the CV industry bore.

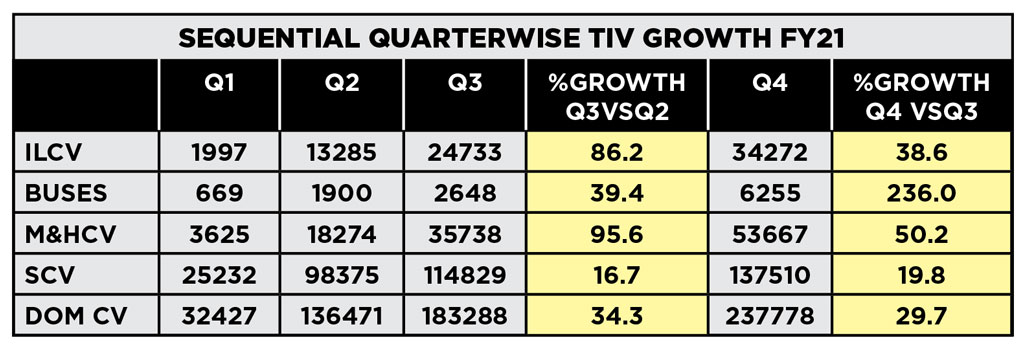

The domestic CV industry volumes were the lowest since FY2010-11 and the most extensive damage was faced by the bus segment. The M&HCV segment followed. In fact, the bus segment led (largest contributor) the industry to record a decline of 17.3 per cent on a YoY basis. The Sequential Quarterwise TIV (Total Industry Volume) growth FY21 chart provides an insight into how the TIV evolved through the year. Barring the bus segment, the industry sales volumes started picking up from October 2020.

Supported largely by the rise in home deliveries of groceries and other essentials, SCVs were the quickest to ride into the positive territory. Through much of the last financial year, the decline in sales was benign (compared to other segments) on a YoY basis. The e-commerce segment that rode the logarithmic rise in online shopping was one of the primary contributors to the growth of the I&LCV segment. The new axle norms meant that a 16-tonne GVW ICV

Supported largely by the rise in home deliveries of groceries and other essentials, SCVs were the quickest to ride into the positive territory. Through much of the last financial year, the decline in sales was benign (compared to other segments) on a YoY basis. The e-commerce segment that rode the logarithmic rise in online shopping was one of the primary contributors to the growth of the I&LCV segment. The new axle norms meant that a 16-tonne GVW ICV  segment vehicle could flaunt a payload of over 11-tonne. It could also boast of a cargo body of up to 31 feet, ideally suited for volume rich consignments of the e-commerce segment for interstate logistics – at higher speeds (faster TAT) and with an optimal TCO when compared to the erstwhile 4×2 vehicles with a 16.2-tonne GVW. Powered by six-cylinder engines, these would also sip more fuel.

segment vehicle could flaunt a payload of over 11-tonne. It could also boast of a cargo body of up to 31 feet, ideally suited for volume rich consignments of the e-commerce segment for interstate logistics – at higher speeds (faster TAT) and with an optimal TCO when compared to the erstwhile 4×2 vehicles with a 16.2-tonne GVW. Powered by six-cylinder engines, these would also sip more fuel.

To motivate, to innovate

To motivate, to innovate

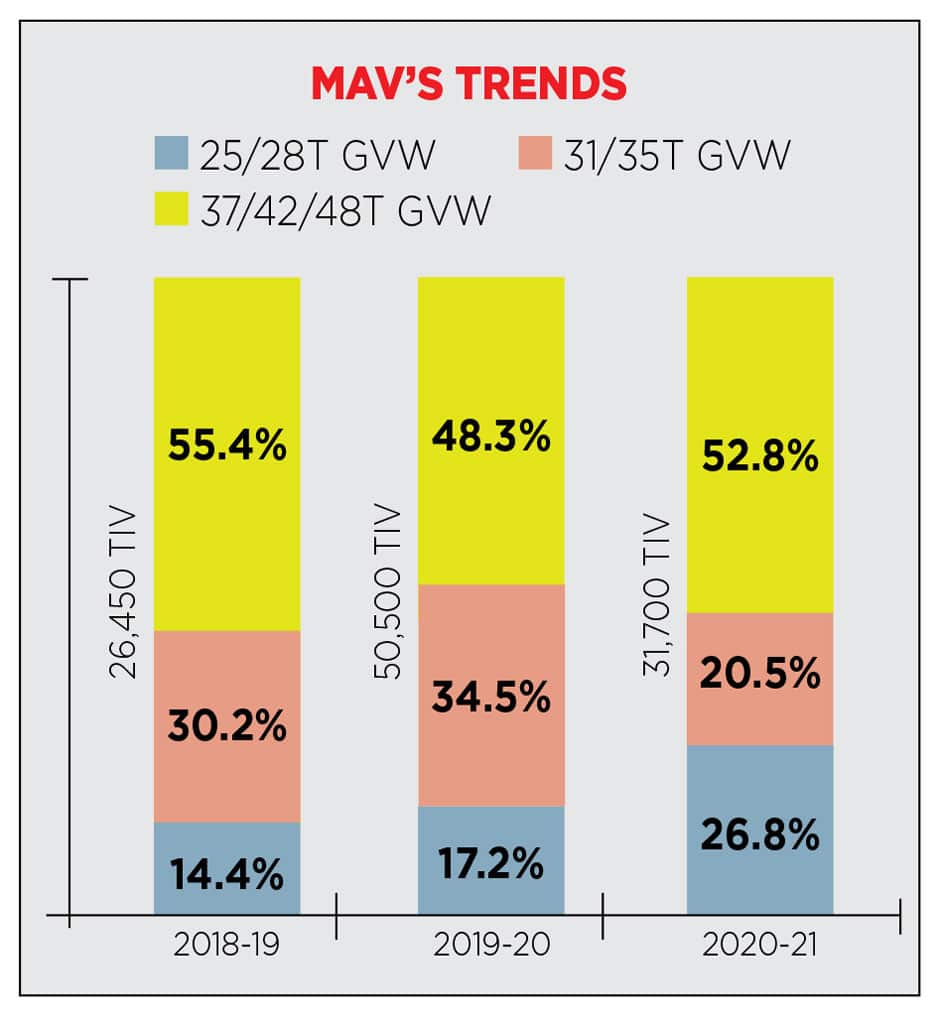

Keeping itself motivated and continuing to innovate, the CV industry in FY2021-22, witnessed the Multi-Axle Vehicles (MAVs) under the HCV segment getting severely impacted. The reason was attributed to the fall in demand. Truck fleet utilisation, in fact, never exceeded 75 per cent. Significant price hike

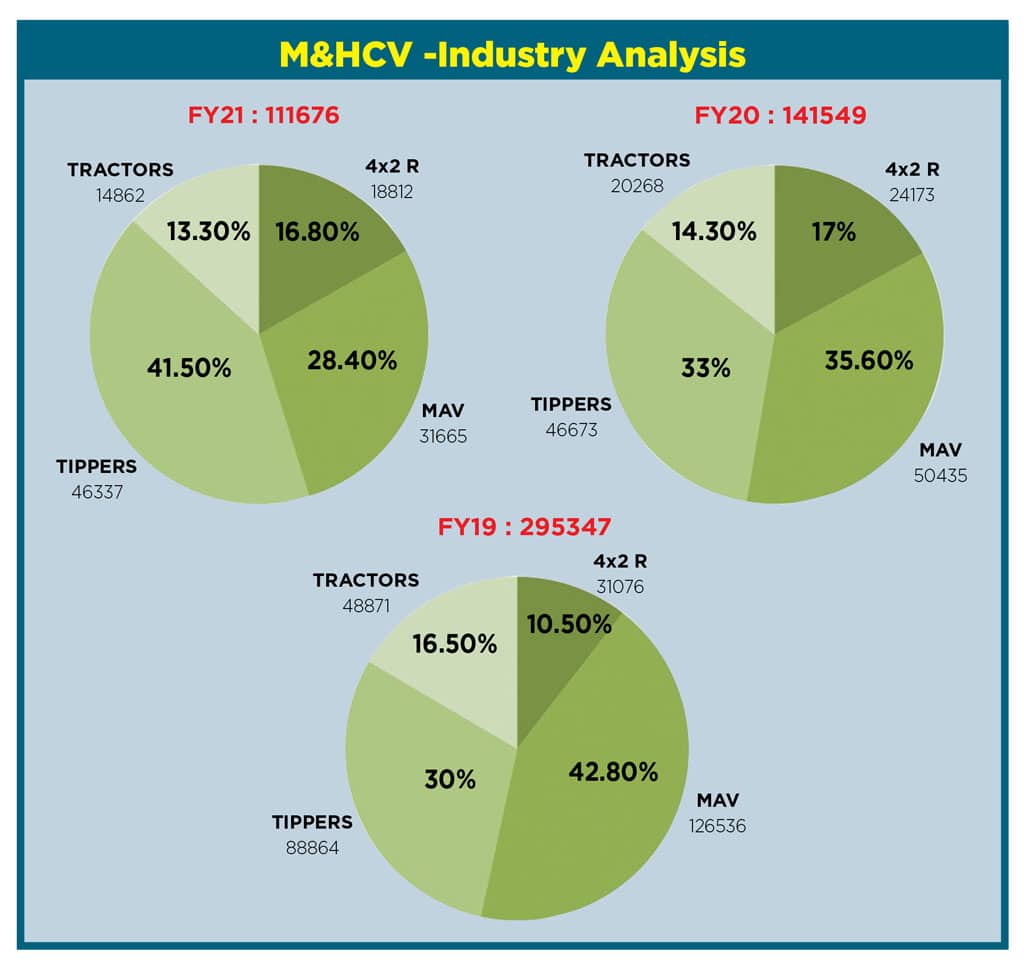

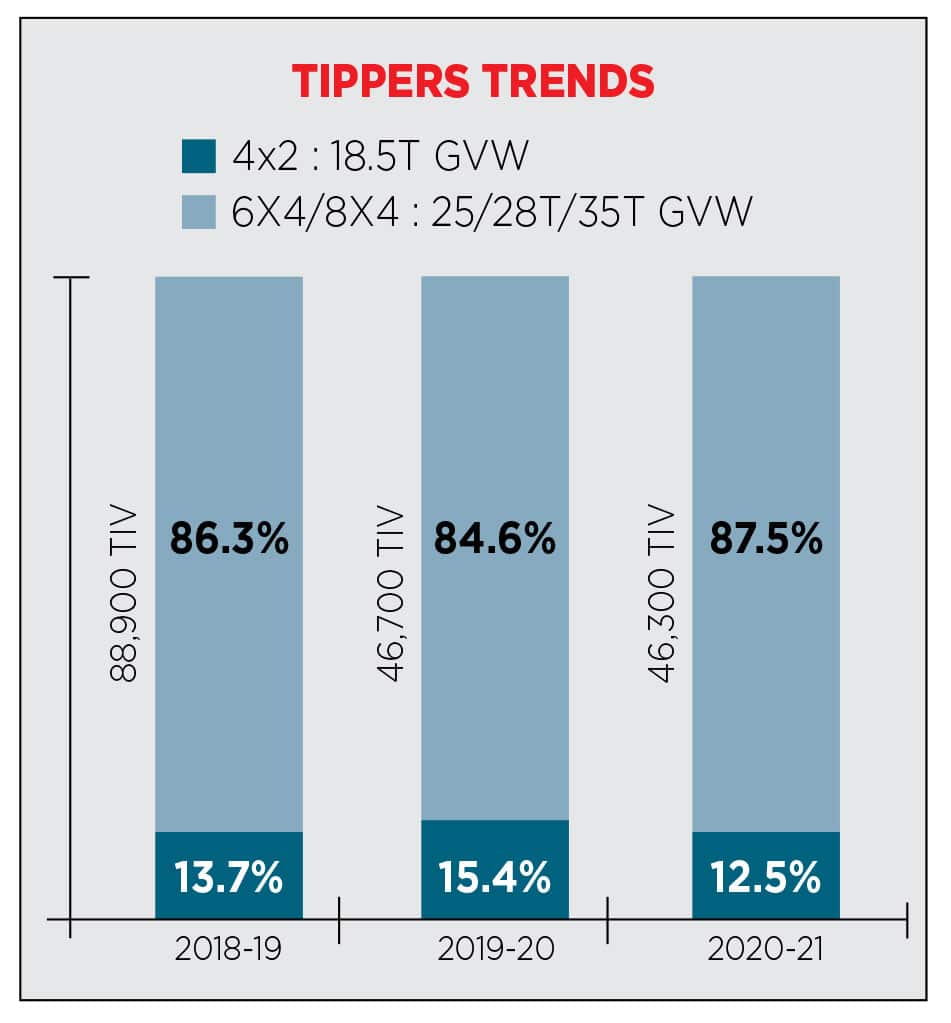

(18-20 per cent) accompanying BSVI transition dampened the environment. Other costs, which would push the TCO up, compounded the situation. Many buyers turned to used and repossessed BSIV CVs as financiers reduced the LTV (Loan To Value) for new vehicle purchases. The tipper segment (consisting predominantly of multi-axle tippers) solely bolstered the M&HCV segment. It contributed 41.5 per cent of the TIV as compared to 33 per cent in FY2019-20.

M&HCV -Industry Analysis

The ‘M&HCV – Industry Analysis’ graphics clearly indicates how and what the CV industry segments were like in FY2020-21. The other graphics, ‘MAV Trends’ provides an insight into multi-axle vehicle trends. The shift to higher GVW vehicles – particularly the 42/48T GVW trucks, point at the ‘Hub & Spoke’ transportation model. The phenomenon gained currency in FY2020-21 some more.

It also contributed to better economics in terms of lower cost per tonne km. The graphics concerning tippers – ‘Tipper Trends, underlines the rising usage of multi-axle tippers, namely of 6×4 and 8×4 axle configuration. Ready Mix Concrete CVs (built on multi-axle tipper platform) became all-pervasive in the construction section in FY2020-21. They too figure in there.

The bus segment was almost vaporised as the fear (Covid induced the need for social distancing) of infection kept masses away from almost any form of shared mobility. Sales of school, staff and tourist buses took a hit. Also that of buses and chasses procured by STUs. Ditto for buses/chasses procured by STU’s. If the lockdown had an advesre effect in the first half of FY2021-22 on public transportation; on intra-city and inter-city buses, the second half did not yield any particular gain either. It, in fact, indicated that the return to pre-Covid levels will take years. I&LCV Industry Analysis

I&LCV Industry Analysis

Particularly in the eight to 16-tonne GVW range, the going was surprisingly as well as fortunately good. The eight to 16-tonne GVW vehicles from the I&LCV segment witnessed good traction on the basis of e-commerce boom and an uptick in some other traditional segments like perishables (fruits and vegetables, dairy and poultry products, and a few others). ICVs reigned supreme on inter-city and regional routes because of their ability to deliver on speed, fuel efficiency and reliability. For time sensitive cargo deliveries, ICVs proved to be the most preferred vehicles in FY2020-21.

Particularly in the eight to 16-tonne GVW range, the going was surprisingly as well as fortunately good. The eight to 16-tonne GVW vehicles from the I&LCV segment witnessed good traction on the basis of e-commerce boom and an uptick in some other traditional segments like perishables (fruits and vegetables, dairy and poultry products, and a few others). ICVs reigned supreme on inter-city and regional routes because of their ability to deliver on speed, fuel efficiency and reliability. For time sensitive cargo deliveries, ICVs proved to be the most preferred vehicles in FY2020-21.

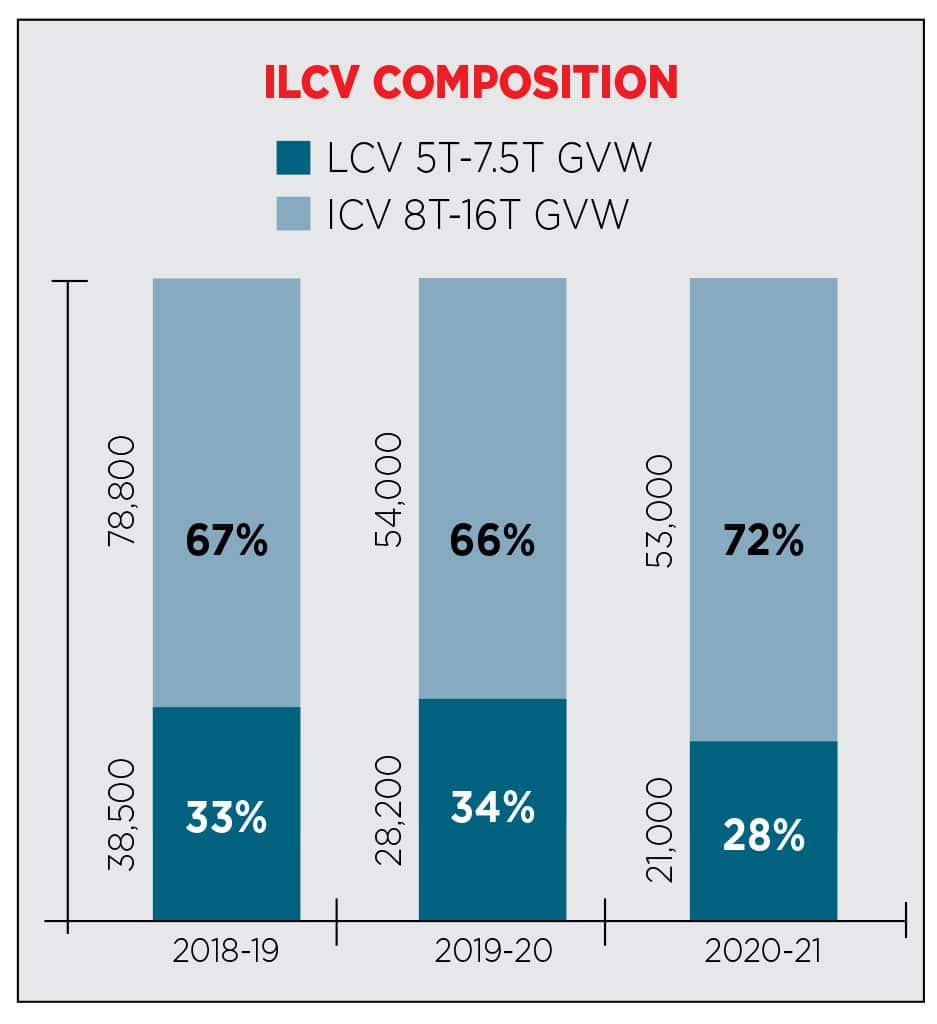

An insight from the study of five to 16-tonne GVW vehicles pointed out that the share of eight to 16-tonne GVW vehicles in the I&LCV segment rose from 66 per cent in FY2019-20 to 72 per cent in FY202021. A look at the chart – ILCV composition, and it will be clear at once. Interestingly, the share of CNG trucks in the I&LCV segment increased by double digits. It could be attributed to hefty price escalation of diesel fuel in a short time and the expansion of CNG network. Used to cover a radius of 200 kms roughly, CNG trucks in the five to nine tonne GVW category were once the most sought. That trend, it looks like, has now shifted to the 12 to 16-tonne GVW category. These trucks are typically used for regional distribution.

Finding new ways to conduct business

The good performance of some of the CVs during FY2020-21 could be credited to the resilience and motivation displayed by their manufacturers. The entire CV industry, in fact, found new ways to work. Against a hostile atmosphere of fear and uncertainty as the pandemic spread its tentacles, shuttering all businesses, manufacturing facilities and service industries in one sweep, the CV industry refused to give up. Despite being badly impacted, it made sure that the country’s supply chain did not collapse.

displayed by their manufacturers. The entire CV industry, in fact, found new ways to work. Against a hostile atmosphere of fear and uncertainty as the pandemic spread its tentacles, shuttering all businesses, manufacturing facilities and service industries in one sweep, the CV industry refused to give up. Despite being badly impacted, it made sure that the country’s supply chain did not collapse.

If the sudden emergence of Covid in India, and the ensuing lockdown saw companies across sectors and their managements go into a huddle, the CV industry steadfastly charted plans and strategies to ride out of the gloomy situation. It re-imagined, re-jigged, revived and restarted plants and processes quickly after the lockdown without violating the guidelines put in place by the governments. It put SOPs in place, re-activated its supply chains, re-engaged with the employees and even provided fiscal relief where it was found to be necessary. Under the overarching umbrella of safety and health protocols across manufacturing locations, supplier facilities as well as in the sales and marketing organisation besides dealerships, the CV industry embraced digitalisation. Switching to digitalisation across the entire value chain, the CV industry found a way to regenerate demand.  It found a way to engage with customers and dealers. Social Media, email marketing, virtual Zoom meetings, mobile apps., WhatsApp and the web transformed into the primary channels of communication. These methods improved customer experience by increasing the response speed to complaints or any other queries. Seeking higher profit and cost control by trimming travel and conventional marketing media spends, the CV industry discovered new means of enhancing productivity and optimising EBITDA among others. Quickly adapting to hybrid work-from-home ways of working, the CV industry successfully tackled the weak link exposed by the pandemic too. The industry also witnessed dealers exiting business due to financial indiscipline.

It found a way to engage with customers and dealers. Social Media, email marketing, virtual Zoom meetings, mobile apps., WhatsApp and the web transformed into the primary channels of communication. These methods improved customer experience by increasing the response speed to complaints or any other queries. Seeking higher profit and cost control by trimming travel and conventional marketing media spends, the CV industry discovered new means of enhancing productivity and optimising EBITDA among others. Quickly adapting to hybrid work-from-home ways of working, the CV industry successfully tackled the weak link exposed by the pandemic too. The industry also witnessed dealers exiting business due to financial indiscipline.

Desperate times, extraordinary deeds

Through extraordinary deeds of supporting fleets by means of emergency repair and service, the CV industry earned new-found admiration for itself. The teams at dealerships braved the whimsical rules and behaviour of the local and regional authorities despite the necessary permissions. The OEMs stood by their dealers and other stakeholders. Some of them even went to the extent of helping dealers to retain employees through incentives. They hand held the dealers by quickly rolling out interest subsidies on vehicle and parts inventory. Watching an uptick in rural economy (on the back of a good monsoon) lead to a surge in tractor demand, the CV industry hoped that the effect will rub on it too. Not the one to be de-motivated, it quickly responded to the effect of vibrant rural markets in terms of the demand for SCVs, LCVs and ICVs.

To an extent, it helped offset the sales lethargy in urban areas. The exponential growth in online shopping and essential deliveries post the lockdown in FY2020-21 led to the CV industry witness an uptick in SCVs, LCVs and ICVs too. e-commerce players like Amazon, Flipkart, and their logistics partners like Delhivery scaled up their operations. They turned to new start-ups and retrofitment companies to address their demand for zero emission urban delivery mediums.

To an extent, it helped offset the sales lethargy in urban areas. The exponential growth in online shopping and essential deliveries post the lockdown in FY2020-21 led to the CV industry witness an uptick in SCVs, LCVs and ICVs too. e-commerce players like Amazon, Flipkart, and their logistics partners like Delhivery scaled up their operations. They turned to new start-ups and retrofitment companies to address their demand for zero emission urban delivery mediums.

Excess freight capacity due to low fleet utilisation coupled with BSVI price escalation put a lid on M&HCV long-haul multi-axle segment almost. Instead, used trucks companies saw their transactions rise with sales from either trucks surrendered by transporters or repossessed by financiers. The multi axle tipper segment came to be the main stay of the M&HCV segment in FY2020-21. It accounted for 41.5 per cent of the total M&HCV’s sold in the respective fiscal. Battling slowdown in sales since Q2 of FY2019-20 and also successfully executing BS VI transition, commercial vehicle manufacturers were forced into emergency response mode in FY2020-21. Without transgressing the safety protocols and guidelines in place, OEM’s had to find ways to address the market needs and compete. New Product introductions like the Bharat Benz 5228TT, Ashok Leyland Bada Dost, Tata Signa 3118.T and Ashok Leyland AVTR 4120 reflected this quite effectively. If the sequential month-on-month growth in high frequency indicators like GST collections, electricity consumption and the PMI (Purchasing Managers Index), which has been consistently been above the 50 mark, indicated economic resurgence in the fourth quarter of FY2020-21, the rearing of the ugly head of Covid once again and with renewed ferocity, the FY2021-22 has begun on a disruptive note. Severel regions and states have announced lockdowns, either fully or partially.

Looking ahead

The spike in Covid infections and related deaths arising from the 2nd Wave, is a worrying development for the economy as well as the CV industry. It has brought with it signs of much disruption, and enough to spoil whatever progress was made in the last quarter of FY2020-21. The first quarter of FY2021-22 will be an extremely challenging if not a wash-out (as it appears now). It is very likely to be extenuating. Against the potential damage to lives and livelihoods caused by the second Covid wave, it will need to be seen how the growth oriented Union Budget (presented on February 01, 2021) stays on course. It marked several measures and outlays for the Construction and Infrastructure sector in terms of providing an impetus to the nation’s economy. As a reflection of a nation’s economy, any change is certain to rub off the transport sector and the CV industry as a whole. Challenges like rising retail price inflation, IIP (Index of Industrial Production) trajectory, unemployment, petroleum prices, high commodity prices and material shortage, a pandemic that does not seem to go yet, there is no doubt that the CV industry will have to motivate itself some more. It will have to also innovate some more. Be sensitive and accommodating of the fact that gross fixed capital formation that is key to GDP growth is virtually non existent. In the short-term, it will be the government capex on infrastructure that will be the savior for the CV industry.